As the potential of open financial protocols becomes clearer, some applications are gaining adoption faster than others. Maker dominates in terms of value locked and volume transacted. Compound and Uniswap trail, but are well ahead of 0x, Dharma, Augur, and dydx when it comes to liquidity. The rest have yet to show up on the radar. Looking at the three dominant protocols reveals a design advantage with respect to liquidity: none of them require users to find a specific peer to take the opposite side of a trade.

The success of Maker, Compound and Uniswap seems to have little to do with the range of use cases they enable. From a lending standpoint, there’s no type of loan that Maker or Compound can offer that two peers can’t at least approximate by trading with each other on Dharma. Through scalar markets, Augur can offer levered long exposure to ETH similar to what one can get using Maker, but with many more options for users. Uniswap has fewer pairs than many 0x relayers, but significantly more trading volume.

Why are protocols that offer fewer options gaining more adoption? It might be because they constrain the types of trades available to users, allowing an “automatic supply-side” to consistently offer the service.

Take a binary market on Augur: to go long ETH a user needs to purchase a long ETH share—a bespoke ERC20 token—from another user or market maker. Or, they can issue themselves a complete set of one long and one short share and subsequently sell off the short token to another user, keeping the long token to themselves until the market settles. These tokens have no pairs on any DEX, much less any centralized exchange. Liquidity for such long-tail assets is severely limited, making it more expensive and less convenient to trade them.

In Maker, the process is much easier to complete. Users issue themselves dai by locking ETH. To go leveraged long, they simply need to exchange their newly-issued dai for ETH, which is easy to do, with plenty of liquidity on any number of exchanges. In other words, Augur fragments liquidity across a large number of unique ERC20s, while Maker concentrates liquidity in a single asset, dai. Augur is a bespoke and varied process, Maker is automatic and consistent. This greatly improves both cost and usability.

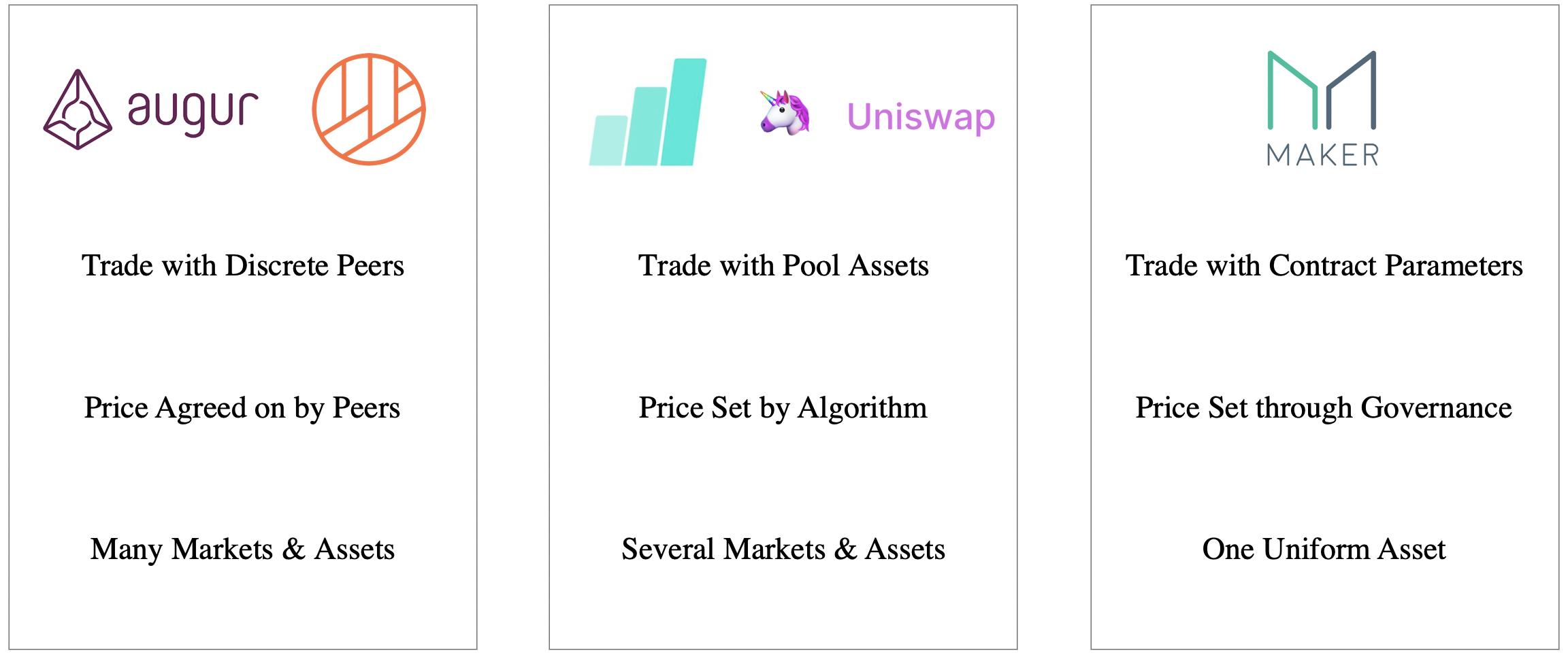

Looking at DeFi protocols from this liquidity angle, three categories are apparent:

One group (Augur, 0x, Dharma) requires users to find peers to trade with, another (Compound, Uniswap) pools maker assets and offers them to takers for a fee, and a final category (Maker) sets parameters through governance, allowing users to trade directly with a smart contract.

Protocols like 0x, Augur, and Dharma are genuinely P2P: For every user that wants to go long, a discrete counterparty must be found to go short. As these are bilateral exchanges negotiated by peers, the types of trades on P2P protocols should form a strict superset of the other categories. There isn’t a universal price, just a series of bilateral trades at different price points (from which we can usually define some notion of implied global price). The types of trades these peers can negotiate with each other has few theoretical limits.

Continuing with a gaming analogy, we can think of Uniswap and Compound as MMORPGs: Instead of discrete bilateral exchanges, all users play on the same map. Users don’t need to find a counterparty, they can just trade with the asset pool. Global prices for those trades are set algorithmically, via a constant product rule in the case of Uniswap and an interest rate model based on utilization in the case of Compound. The set of trades and markets is more constrained.

Maker offers a (quasi) single-player mode, where users issue themselves loans subject to parameters decided through governance (one could argue that users trade with a pool that represents governors of the system). Currently, there is only one type of trade offered and liquidity is concentrated in one asset, dai.

On Augur, any user can create long exposure to any event, as long as they find a peer to take the opposite side. On Dharma, anyone can borrow any asset on any terms, as long as they find a peer to lend to them. On Maker, the array of “bets” one can take is smaller, but once set, there’s little liquidity constraint—ie. single-player mode is possible (subject to online parameters). In the case of Maker, this means the core team only has to focus on creating demand and liquidity for dai, as opposed to an entire infrastructure for multi-asset exchange.

We’ve observed over the last few months that protocols that concentrate liquidity into a smaller number of markets and assets have thus far had a much smoother path to adoption. Development teams behind P2P DeFi protocols have taken note. The Dharma team has moved “up the stack” to create a Dharma application called Lever, which has already overtaken the protocol’s original P2P lending volume. One thing to notice is that Lever has constrained the product set, allowing borrowers and lenders to concentrate liquidity into a smaller number of loan types. To address the P2P liquidity problem head on, the 0x protocol team has shifted its focus from relayers to market makers.

That said, many of these P2P protocols still require more infrastructure to scale, a headwind that affects their limited-choice counterparts less. For example, mechanisms for peers to find each other (notice that Dharma, Veil/Augur, and 0x all incorporate some notion of a “relayer”), market makers to solve the double coincidence of wants, and scaling solutions to efficiently settle large numbers of independent trades.

If the DeFi community figures out liquidity solutions for the long-tail assets (such as non-fungible tokens and prediction market shares), P2P protocols may well outpace the utility of their less flexible analogues by offering the “endless aisle” of asset types and custom exposures. These peer-negotiated contracts can theoretically allow users exposure to any asset or state of the world. Such plasticity may allow these systems to serve increasingly deeper niches as the flywheel of market completeness kicks in.

Aggregated or automated supply-side protocols are coming from the opposite direction. For example, Maker intends to expand its product set through multi-collateral dai and Uniswap will likely continue to expand its pairs, though both networks will have to remain mindful of fragmentation trade-offs for liquidity.

While it’s as of yet unclear who will be the ultimate winners, networks in both categories appear to have their sights set on offering a broad selection of markets with adequate liquidity for users. For now, the ones that have built deep liquidity in a handful of important markets appear to have the adoption lead.